Summer 2024

—Adrian G. Davies, CFA — President

In the first half of 2024, a handful of stocks with large weightings in the S&P 500 Index performed very well, leaving most of the rest of the index constituents underperforming. The S&P 500 Index returned 15.3%, with the seven largest names in the index returning about 31.5% collectively, accounting for 62% of the gains for the entire index, while the “other 493” returned an estimated 7.7 percent. The Invesco S&P 500 Equal Weight ETF (RSP), indicative of what the average S&P 500 stock has done, returned 5.0% year-to-date. The Russell 2000, an index of two thousand smaller-capitalization stocks, was up 5.2% through March, before falling 3.3% in the second quarter.

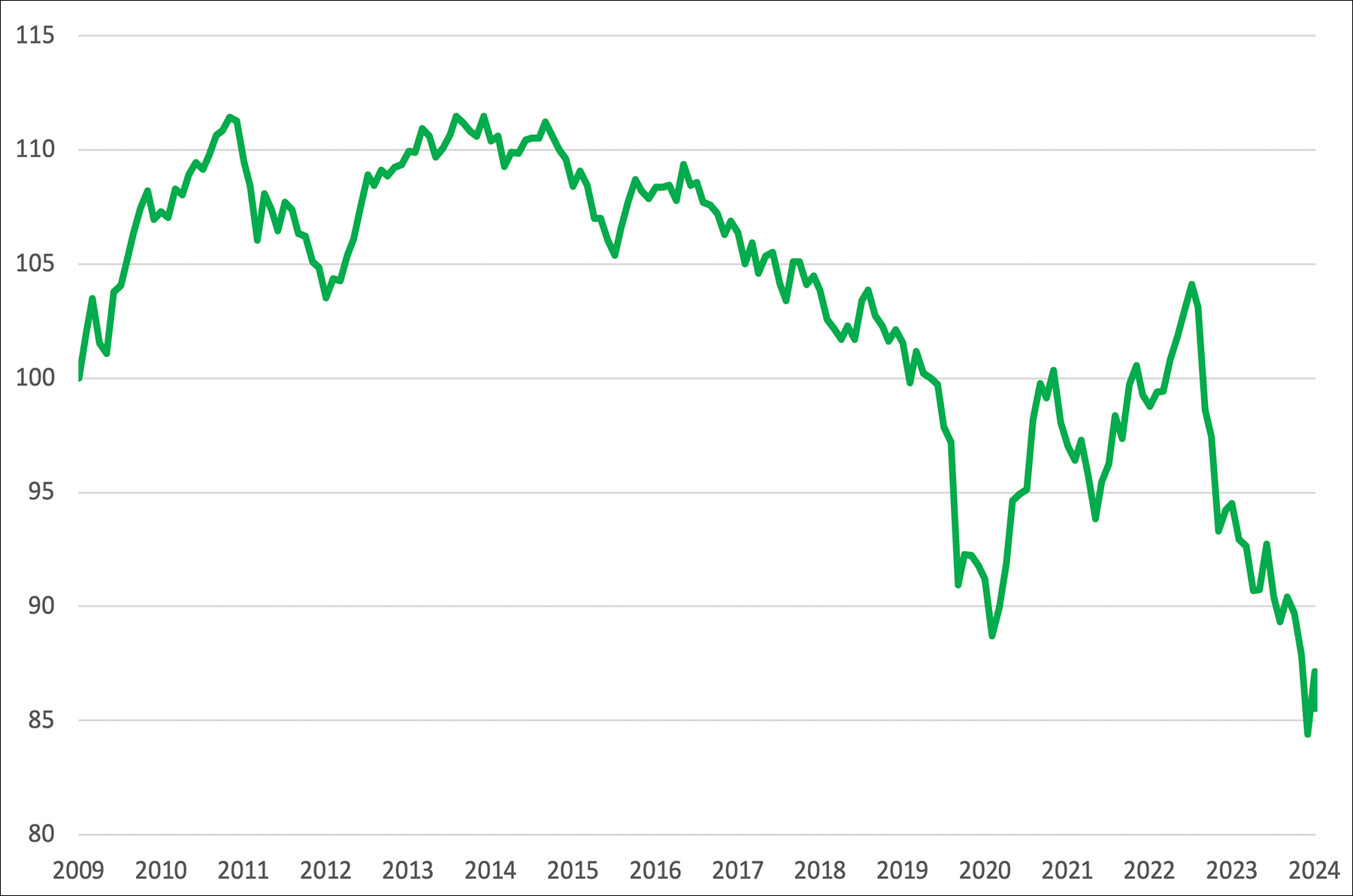

While some smaller-capitalization stocks also did exceedingly well, it is the largest S&P 500 constituents that have been roiling portfolio managers’ relative performance. With the S&P 500 Index constituents’ weightings based on market capitalization,[1] the largest stocks are often important contributors to performance, but seldom do they outpace the average stock by such a large margin as is evidenced in Chart 1. The cumulative results of this performance differential since 2014 can be seen in Chart 2. When the largest stocks are outperforming the index, active managers are challenged not just to pick the right stocks, but also to hold them in sufficiently large positions relative to the index. The seven largest companies made up 33% of the index halfway through the year. Investors focused on short-term performance and those with “Fear of Missing Out” (FOMO) are compelled to buy still more of these large-cap winners, driving them still higher in a self-reinforcing cycle. Whether or not active managers intend to maintain such concentrated portfolios, they are under increasing competitive pressure to do so.

The current narrow breadth also suggests greater vulnerability to a market downturn. With such a high concentration in so few names, a change in thinking towards one or more of these large-cap stocks could move the index downwards. Changes to the economic backdrop could also change market dynamics: the economy could speed up or cool down, or inflation could reaccelerate. With inflation continuing to moderate, the hope is that the Federal Reserve will cut interest rates, stimulating the economy and broadening participation in the bull market. Smaller-capitalization stocks started rallying in July.

Chart 1. Invesco S&P 500 Equal Weight ETF Y/Y Return Minus S&P 500 Index Y/Y Return

Source: FactSet data

Chart 2. Cumulative Invesco S&P 500 Equal-Weight ETF Relative to S&P 500 Index – Total Return

Source: FactSet data

Source: FactSet data

The Magnificent Seven

The club of elite large-capitalization stocks is subject to continual revision. The seven largest stocks in the S&P 500 Index, dubbed the Magnificent Seven (Microsoft, Nvidia, Apple, Amazon, Alphabet, Meta Platforms, and Tesla)[2] evolved from the “FANG” stocks (Facebook, Amazon, Netflix, and Google), with Wall Street and the financial press the arbiters of whatever group name sounds catchy at the time. Because “magnificent” has too many syllables, some have already shortened the moniker to “Mag-7.”

The Magnificent Seven have strong fundamentals, although Tesla is arguably an exception. The other six seem to be natural monopolies or oligopolies, benefiting from scale and networking effects. They have strong profit margins and they are global. We estimate that the Magnificent Seven accounted for more than 100% of the total growth in S&P 500 earnings last year (earnings for the rest, in aggregate, declined),[3] and Magnificent Seven earnings are expected to account for 50% of total S&P 500 earnings growth this year. This would suggest that the relative strength in Magnificent Seven shares is at least somewhat justified. Stock performance won’t necessarily “revert to the mean” with smaller stocks catching up to their larger brethren. Corporate earnings growth would likely have to broaden out in order for the July small-cap stock rally to be sustained.

When the Federal Reserve started raising rates in 2022, the market’s initial reaction was to punish the Magnificent Seven. Because interest rates are used to translate future forecast cash flows into present values, higher rates should make these growth stocks, whose values are more dependent of future cash flows, sell off more than other stocks. However, these large-capitalization stocks have also been more insulated than other stocks from economic pressures. Being primarily digital companies, and dominant in their industries, they weren’t particularly squeezed by inflation. While they have continued to report strong growth, the stabilization of interest rates over the last year has helped to springboard their stocks higher. Inflation seems to be in abeyance for now —that could help real economy stocks that have been squeezed by inflation.

Enter Artificial Intelligence

AI is the market’s latest fascination. Although AI has been under development for decades, the public and business leaders caught on to its massive potential after OpenAI introduced Chatbot GPT in November 2022. Many investors expect it to be as transformational as the internet itself, with the Magnificent Seven building on their dominance as large technology companies to make the most of the opportunities it presents.

AI learns from complex data sets to the point where it can mimic human responses, create artwork, and detect patterns unrecognizable to most humans. Large language models provide a more natural way to interact with computers, and the technology can reduce or eliminate most rote data processing tasks. In a KPMG survey of businesses with over $1 billion in revenue, 43% said they plan to invest $100 million or more in AI over the next twelve months.[4] Financial technology provider Klarna said that its AI system can do the work of 700 call center agents. There are also numerous national security applications, from autonomous drones and computer hacking to battlefield simulation. AI combined with robotics will open up a new vector for growth.

AI has its challenges, such as hallucinations (errors), offensive content, harmful biases, copyright infringement, and regulatory issues. The optimists believe these problems can be solved with bigger and more elaborate AI systems. AI is here to stay—we just don’t know how large the industry will be.

AI processing requires the buildout of massive new data centers, and the volume of data processing requires massive amounts of energy. Data centers are expected to almost double their energy consumption globally, to 800 terawatt-hours, by 2026.[5] The rollout of AI might not be constrained by demand for AI processing, but rather by the availability of the energy sources necessary to run the data centers, limiting the industry’s growth.

Nvidia dominates the market for AI semiconductors. Investors are betting that the other Magnificent Seven stocks will profit from offering AI services to others, although it will take time before these investments are able to contribute to corporate profits. Particularly in the context of a narrow, momentum-driven market, it is reasonable to look at the market leaders with some caution. The Magnificent Seven stocks are expensive relative to their own trading histories. On the other hand, reliable cash flows and AI are possible reasons why higher valuations might be justified. Weakening of economic growth from here could mean quality growth stocks maintain their premium valuations: when growth is scarce in the face of a weakening economy, investors tend to bid up the few remaining reliable growth stocks, abetted by the potential for lower rates.

The Technology Bubble of 2000

Today’s AI boom may look similar to the technology bubble of 2000, when the emergence of the internet captured investors’ imagination. Stock market breadth narrowed during that period, as investors sorted the internet winners from the losers. Just as industries’ ability to commercialize AI remains unproven today, the profitability of internet investments remained in doubt a quarter century ago. Just in case anyone was wondering about the implications of the name, the movie The Magnificent Seven does not end well for the seven heroes.

In 2000, Wall Street anointed “the Four Horsemen”—Microsoft, Intel, Cisco Systems, and Dell. For the most part these tech companies are still dominant forces within their industries, but since the bubble, their stocks have been on different trajectories, with Microsoft becoming the most successful of the four. Investors drove Microsoft’s stock up to a P/E of 67 times prospective earnings in 1999. The company went on to compound earnings 13% per year through the 2000s, and yet the stock had been bid up so much during the tech bubble that it underperformed during the decade of the 2000s. Microsoft has since regained its footing, growing through the 2010s and 2020s to become the largest company in the world, in part due to its adroit foray into AI. Microsoft stands in comparison to Cisco Systems, which traded as high as 126 times earnings in 2000, fell harder, and has been growing more slowly since.

Many “dot-com” companies from that era went bankrupt. Amazon has probably become the most successful dot-com company: after falling 92% in the aftermath of the tech bubble, its stock has compounded at a rate of 31% per year. Generating losses, it did not have a P/E until 2002, and it has persistently traded at a high multiple ever since.

Is Magnificent Nvidia in a Bubble?

To many, AI market leader Nvidia looks to be at the center of a bubble. The stock has shot up quickly. Nvidia now is a $3 trillion market capitalization stock, having risen 149.5% in the first half of this year, after having risen 239.0% in 2023. It recently represented 6.6% of the S&P 500 Index, on par with Apple (6.6%) and Microsoft (7.3%). For comparison, the Russell 2000, an index comprised of two thousand smaller-capitalization public companies, had an aggregate market capitalization of about $3 trillion. We recognize the stock trajectory as something that happens during bubbles, but if AI stocks are in a bubble, it’s a different sort of bubble. Nvidia’s operating results have exploded commensurately with its share price.

Nvidia’s fate will be determined primarily by the sustainable size of the market for AI chips and its market share. The industry should continue to see secular growth as the technology improves and is adopted in more and more applications. As of this writing, the market is still expanding at a rapid clip, with Nvidia selling $22.6 billion worth of AI chips in the first quarter of the year. The market is also likely to be cyclical, as companies’ proclivities to invest are dictated by their own business cycles. AI is arguably driving this business cycle. If there is a bubble, it’s because thousands of professional managers have chosen to invest billions of dollars in AI. The investment craze may yet cool down.

About half of demand for AI chips comes from the hyperscale data centers. These data centers, run by Amazon, Microsoft, and Alphabet, among others, are reselling AI services and AI compute capacity to others. They are each developing their own in-house AI semiconductors, which will take some market share from Nvidia over time. However, Nvidia has the advantage of being platform agnostic, with each of these large competitors likely limited by their own platform.

Like many other technology companies, Nvidia benefits from scale and networking effects. Its development software for AI, CUDA, has become the industry standard. Most AI coders are familiar with it, and troves of programming resources have been developed for it, giving it a huge advantage over those who would develop competing systems. CUDA seems to be critical to Nvidia’s “moat,” giving it a sustainable competitive advantage for a long time to come.

Nvidia could be caught up in geopolitical risks. The company designs chips that are manufactured by Taiwan Semiconductor. China, seeking control of Taiwan, and being in technological competition with the West, could disrupt commerce in Taiwan.

Those with a less sanguine view of Nvidia often cite its valuation, comparing the company to historical sales and earnings. Nvidia recently traded at 37 times the last four quarters’ reported sales and 67 times historical earnings. Looking at prospective forward sales and earnings offers a more charitable view. Sales are forecast to grow 65% for the full year, having grown 262% year-over-year in the first quarter. First quarter earnings grew 462% year-over-year, but of course these rates are expected to slow. The company traded at 23 times prospective four quarters’ sales and 41 times prospective earnings. Such explosive growth makes valuation multiples unreliable. Demand could always wane, but it’s hard to see demand retreating back to 2023 levels. Nvidia trades at a high multiple of sales because it has operating margins in the 65%–70% range. Determining a fair valuation estimate for Nvidia begs a number of questions: What will Nvidia’s growth rate be going forward? Are its profit margins sustainable? If sales and earnings can continue to grow at above-average rates from here, 41 times may not be an irrational multiple of earnings.

While Nvidia still offers much promise, it would be virtually impossible for the stock to post performance comparable to its historical returns. That’s not to say Nvidia and other Magnificent Seven stocks can’t outperform from here, but past success can make it harder to outperform going forward. The company has been exceeding the high expectations set for it, with expectations ratcheting further upwards with each earnings report. At some point, Nvidia will miss the high bar set for it. Every stock has an expectations cycle, although few have done as well as Nvidia.

Even great stocks cycle through optimistic times and pessimistic times. Investors can always get still more optimistic, but the balance of the probabilities would warrant some caution, even if Nvidia has many great years ahead of it, which we think it does. Many prognosticators, including Woodstock Corporation’s Director of Research Tom Stakem,[6] have suspected that the stock market, lopsided in favor of the largest stocks, has been due for a rebalancing in favor of smaller stocks, and that rebalancing seems to have started in July. The peak of the technology bubble in 2000 was a great time to invest outside of technology, particularly to invest in value stocks, even if some of the winners such as Microsoft and Amazon went on to rise again.

Implications for Woodstock Portfolios

We aim for Woodstock equity portfolios to outperform the S&P 500 over the long term, subject to the risk tolerances and capital gain tolerances of each individual client. We tend to manage diversified portfolios of 40–50 stocks, making our client portfolios much more concentrated that the S&P 500 Index. We believe such diversification goes a long way—investors are better served by holding fewer names and watching them closely. The narrow market breadth of the last few years has demonstrated one risk of being over-diversified. We like portfolios with concentrated positions as long as they are positioned in the right stocks, but the current concentration of the S&P 500 Index is forcing many investors who would otherwise have more diverse portfolios to chase the same stocks, helping to drive them upwards. When these stocks eventually disappoint expectations, there will be a great many investors ready to sell. The stocks are likely to become more volatile.

Woodstock clients may or may not own positions in the Magnificent Seven stocks. To the extent that Woodstock clients have owned Magnificent Seven stocks for a period of time, they have likely grown to become larger positions in client portfolios. We believe is it appropriate to trim oversized positions. We are mindful of the taxes incurred when selling successful investments—we try to balance tax sensitivity with our investment objectives of generating strong returns and managing overall portfolio risk for each client.

As Tom Stakem mentioned in our last Quarterly Market Perspectives, the level of market concentration presents both a risk and an opportunity. At some point, the names that have been outperforming will become overvalued, while investors will reconsider the stocks that have been underperforming. That process may have started in July. There are good stocks to be found at reasonable valuation levels. Economic conditions also change, altering the dynamics of which stocks can outperform, substantiating the need for portfolio diversification.

Disclosure: Certain information contained herein has been obtained from third party sources and such information has not been independently verified by Woodstock. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Woodstock or any other person. While such sources are believed to be reliable, Woodstock does not assume any responsibility for the accuracy or completeness of such information. Woodstock does not undertake any obligation to update the information contained herein as of any future date.

This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Specific investments described herein do not represent all investment decisions made by Woodstock. The reader should not assume that securities identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future. A complete list of all securities recommended by Woodstock in the preceding year, a full compliant Global Investment Performance Standard (GIPS) Composite Report, and the list of composite descriptions are available upon request from Woodstock.

Past performance is not indicative of future results.