Fall 2024

—Robert B. Sanders, Senior Vice President and Portfolio Manager

We have often been asked “how should we be positioning our portfolios for the incoming administration?” One can make incremental changes to investments on the margin, tilting a portfolio to favor a particular outcome depending on what policies one expects to gain traction. It is difficult to predict these outcomes with any certainty, and this year has been no different. Therefore, gambling on one or another candidate or party victory generally does not warrant dramatic adjustments to a portfolio. This year, with the odds split on a winner in the months leading up to November 5th, we stuck to owning companies that we expected would prosper under either party’s victor, and would be capable of riding out any short-term volatility from post-election results.

With the election behind us, we are beginning to get a better view of the policy changes and related economic impacts ahead from a second Trump presidency, bolstered by Republican control of the House and Senate. His campaign pledges outline an agenda that on balance we would expect to be inflationary, with interest rates remaining higher for longer, a strengthening US dollar, and a growing national debt.[1] These effects will be economic headwinds of varying degrees, but we believe the outlook for the US economy is still fundamentally strong.

A Solid Economy

The US economy has been on a positive trend by most economic measures leading up to the election this year. According to the US Department of Labor, the unemployment rate has been rising slightly, with some noise in the recent quarter due to strikes and hurricanes, hitting 4.1% for the months of September and October, and relatively stable though fluctuating for the year between 3.7% and 4.3 percent. This is slightly elevated from 2023 levels but low by historical measures. In addition to the positive labor rate, the average hourly earnings of employees on private nonfarm payrolls have increased 4% over the prior twelve months.

The rate of inflation has been falling, with the Personal Consumption Expenditures (PCE) price index trending lower to 1.5% in the third quarter, down from 2.5% in the second quarter. The PCE price index is one of the preferred metrics the Federal Reserve uses in determining the direction of the economy to set monetary policy. The relatively low inflation growth rate today is little solace for consumers who have experienced a 22.4% cumulative increase in average prices per the Consumer Price Index (CPI) since January 2020 according to the US Bureau of Labor Statistics.

In spite of higher prices, and the high level of interest rates on consumer debt and mortgages, record consumer spending is helping drive real gross domestic product growth (real GDP is the inflation-adjusted GDP measure), which increased at a 2.8% rate in the third quarter, down from up 3% in the second quarter (see Figure 1). Although consumer spending, which accounts for more than two-thirds of US GDP, reached an all-time high of $16.1 trillion in the third quarter, high price levels may yet put this resilient spending pattern at risk.

Figure 1 – Real Gross Domestic Product

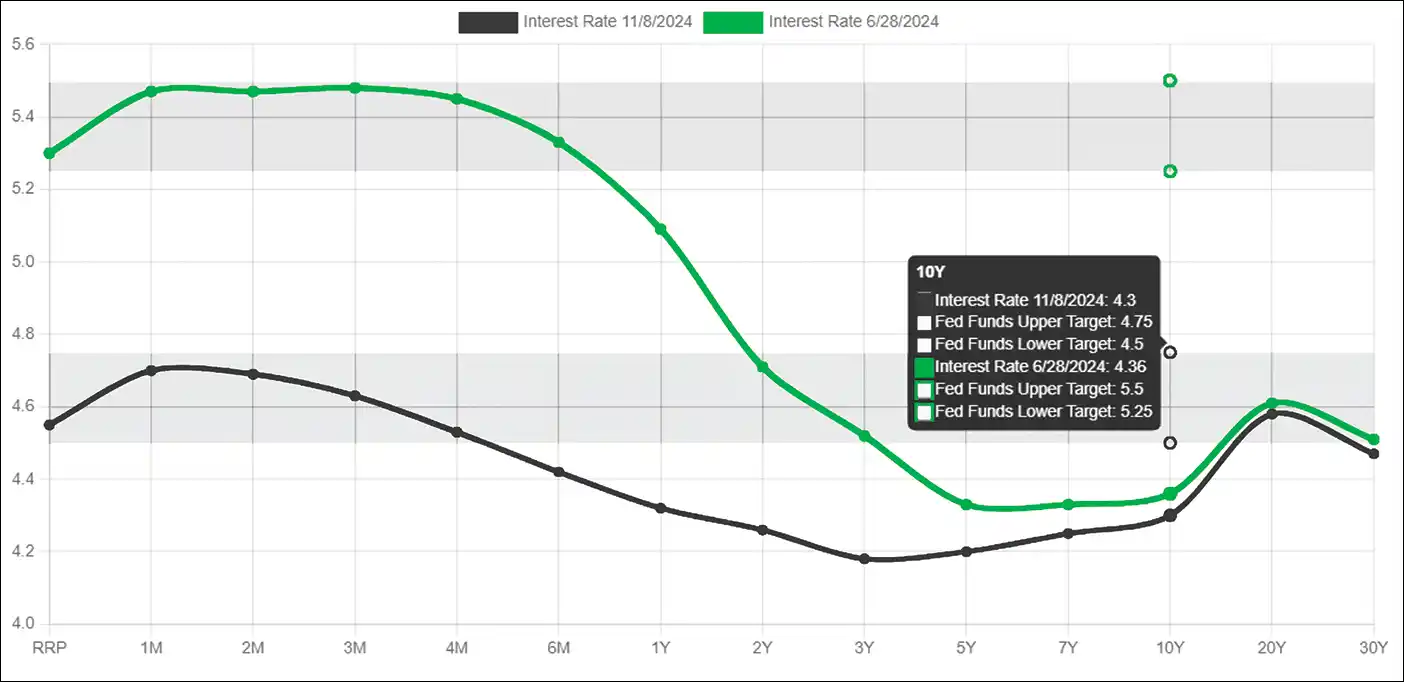

Real GDP, inflation and employment statistics have been trending in the right direction, giving the Fed comfort to cut the target federal funds rate 50 basis points in September to the range of 4.75% to 5 percent. Fed governors followed that decision with another cut of 25 basis points two days after the election in November. This has had the effect of bringing down the short end of the US Treasury bond yield curve, though the curve remains inverted, meaning short-term rates are still higher than intermediate- and long-term rates (see Figure 2). Money market funds invest in the short-maturity end of the fixed income market, holding securities that may mature up to a year ahead, but mostly hold maturities of 90 days or less. Fed rate cuts are bringing money market fund yields lower than the 5% we had been enjoying last year, but a normalizing yield curve should eventually make bond investing more attractive across the range of maturities.

Figure 2 – US Treasurys Yield Curve and Fed Funds Target Range

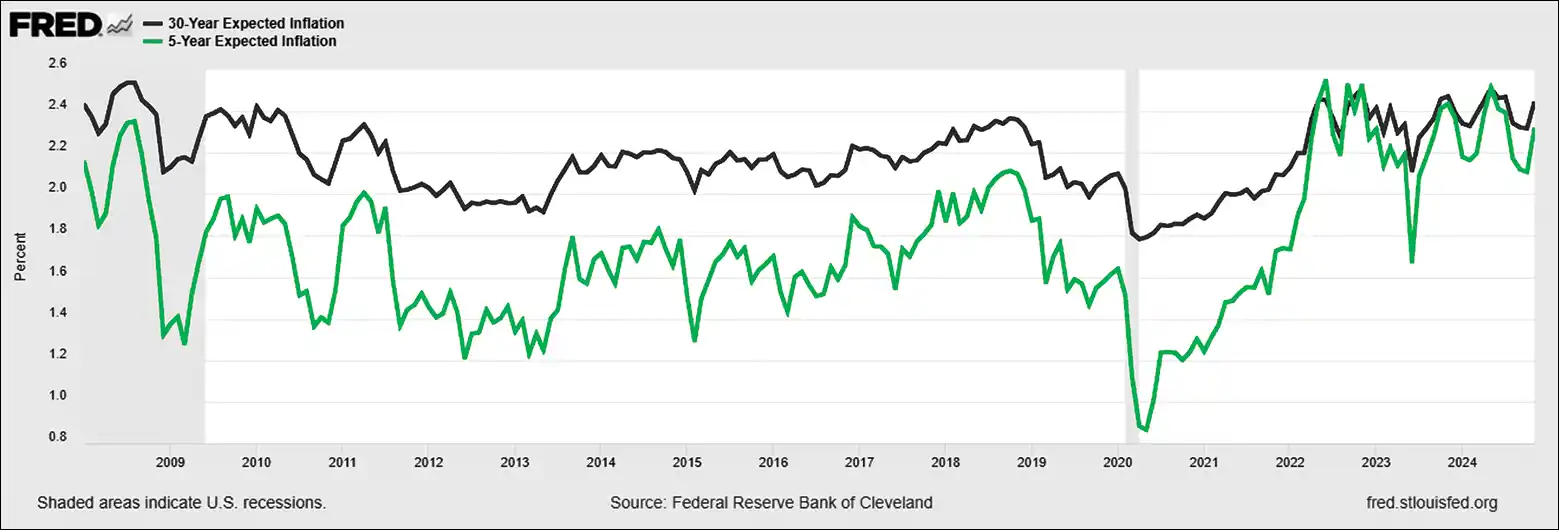

The Fed cuts signal that it believes the economy is not overheating, and that inflation is coming under control, with twin goals of achieving maximum employment and a long-run inflation rate of 2 percent. However, expectations of inflationary impacts of the Trump agenda should slow the frequency and magnitude of Fed rate cuts going forward. The capital markets have yet to price in any dramatic upward shift in near-term (5-year) or long-term (30-year) inflation expectations, which have been anchored in a Fed-friendly 2.2% to 2.5% range since 2022. Long-term inflation expectations have also been in a remarkably stable range since the Obama-era recession ending in 2009 (see Figure 3).

Inflationary Pressures from Policies?

Nonetheless, inflationary economic pressures could develop as the Trump administration policies evolve. Evidence of changing economic expectations was immediately apparent following the election, with public markets driving up bond yields and lowering bond prices. Higher bond yields also influence the attractiveness of US debt abroad, which strengthens the value of the US dollar against foreign currencies. A stronger dollar will generally hurt exporters, since foreign buyers would have to pay more for US goods in their local currency. US dollar strength will typically benefit importers and consumers of imported goods who can buy foreign goods more cheaply. That relative valuation advantage also means importing raw materials and manufacturing components should be cheaper for American companies.

Countering input cost benefits, the strong dollar will make it more difficult for domestic firms to compete with foreign imports on the price of finished goods. A status quo result from the interplay between a strong US dollar making imports cheaper and higher tariffs making them more expensive would be surprising. Across-the-board tariffs may be the more powerful of the two forces affecting prices, all else being equal. The resulting inflation could weaken real consumer spending, dampening economic conditions, and exerting downward pressure on interest rates.

Figure 3 – Inflation Expectations Over Recent Presidential Cycles

What’s Next for Markets?

This backdrop of positive economic trends and a US stock market up 19.6% year-to-date through October, as measured by the S&P 500 Index, naturally prompts the big question of what is next for the economy and investment markets. President-elect Trump touted extending the tax provisions of the 2017 Tax Cuts and Jobs Act enacted during his first term, keeping individual rates unchanged.[2] He has proposed eliminating taxes on tips, overtime pay and Social Security benefits. He also proposed expanding the child tax credit and reinstating the tax deduction for state and local taxes (SALT), and making auto loan interest tax deductible. These individual provisions could help the average taxpayer, potentially buoying consumer spending in light of the higher average prices.

Trump also proposed lowering the corporate tax rate, already at 21%, to 20% or 15% for companies manufacturing products in the US. This pro-business stance helped stage a stock market relief rally after election night. With Democratic plans for corporate tax hikes evaporating, stock market prices gained ground on expectations that average corporate earnings would be higher in the future, bringing market valuations along with them. Lower corporate tax rates could also spur investment, hiring and wage growth for follow-on positive economic growth outcomes.

Tariffs and Interest Rates

Beyond tax policy, President-elect Trump campaigned on a promise of imposing high tariffs on imports from China (60%), and tariffs of 10% to 20% on all other imports. Among his proposals, this policy may have the largest impact on the economy. Tariffs that are not fully absorbed by importing companies would have an inflationary impact on the prices of goods. One study of the tariff proposal concludes average consumers would take the brunt of tariff impacts: “…the Yale Budget Lab estimates consumer prices would rise by 1.4% to 5.1% with a cost per household of $1,900 to $7,600.”[3]

Eventually tariffs may have an offsetting positive effect of encouraging the on-shoring of manufacturing to increase domestic industrial production and boost consumption of domestically produced goods over imports. It is also yet to be determined to what extent trade wars will be prompted by the new tariffs, as much as it would be naïve to assume there will be no countermeasures enacted by foreign market participants. One could surmise that the tariff threat is merely a bargaining ploy by the incoming administration, not intent on sparking a trade war, but to achieve some other objectives. Consensus, however, is the tariffs, if enacted, would dampen consumer spending and raise long term inflation rate expectations.

Long-term inflation expectations impact the level of interest rates, driving them higher for longer. It is not hard to imagine that the affordability of housing, tied to the level of 30-year mortgage rates, would continue to be a challenge in that scenario. Higher rates for auto loans, education loans, and commercial loans would also crimp GDP growth in the future. Trump has indicated he favors lower interest rates, in opposition to the expected results of the tariffs. These are conflicting objectives Mr. Trump hasn’t reconciled, though he would like the executive branch to have some direct influence over the Federal Reserve and its monetary policy, perhaps in an attempt to have his cake and eat it too. The independence of the Fed allows it to act without political interference or agendas, particularly important during election cycles. For now, the Fed is protected from presidential interference, as it is accountable to Congress.[4]

President-elect Trump has advocated for less government regulation, particularly for banks, and mergers and acquisitions. This has been a boost for financial sector stocks in the days after the election. His plans also include rolling back energy sector regulations on fuel and energy efficiency, reducing tax subsidies for green energy and electric vehicles, incenting oil and gas drilling, and paradoxically, expanding carbon capture credits, all of which is resetting energy and climate policy in the US. Additional US energy supply from drilling is unlikely to impact US energy prices dramatically as oil has already dropped 40% from the peaks in 2022, and natural gas prices have already come down over 70% from those highs. However, the energy sector will likely profit from less regulation.

Potent and Disruptive Impacts

Trump’s immigration and border policy, including a plan to deport potentially millions of undocumented people and to limit work and student visas, will have a damaging impact on economic growth, lowering consumer spending, reducing labor supply and increasing labor costs.[5] Many industries depend on immigration to fill job openings, back-filling for retiring baby-boomers, and hiring migrant workers to fill positions in lower income tiers, particularly among agricultural sectors. A limited supply of immigrants may also have an impact on hiring for white-collar jobs, particularly in the technology industry, which is reliant on highly educated foreign workers to sustain growth and competitiveness. However, it is not unusual for companies to outsource technology work to foreign workers overseas at cheaper labor rates than can be sourced in the US. This global off-shoring of knowledge work is not likely to reverse course with Trump policies.

President-elect Trump’s policy agenda is long and diverse among the sectors it could impact. Many of these policies will require legislative actions of Congress to implement — which will take time. Republican control of the US Senate and House of Representatives will make for an easier path to passing Trump’s proposals, but it is not a guarantee he will achieve all of his objectives. Tax acts, energy initiatives, healthcare policy, and influence on the Fed would all require congressional action. Tariffs, immigration, and some regulatory changes can be implemented by executive action, however, so one would expect Trump to enact those policies first following January 20th Inauguration Day. The impacts of these policy changes could be potent and disruptive.

Our investment process astutely monitors, examines and appraises the dynamic economic and geopolitical implications of a changing world for the sectors and companies where we invest. Long-term investing implies looking through relatively short periods, like four-year presidential cycles, as merely short-term influences. Our approach to portfolio management continues to have a foundation of investing in quality companies that we believe can thrive through the economic headwinds and tailwinds of this election cycle. As always, please reach out to your portfolio manager to discuss market expectations and their implications as they apply to your investment portfolio.