Spring 2026

— James H. Garrett, CFA – Vice President

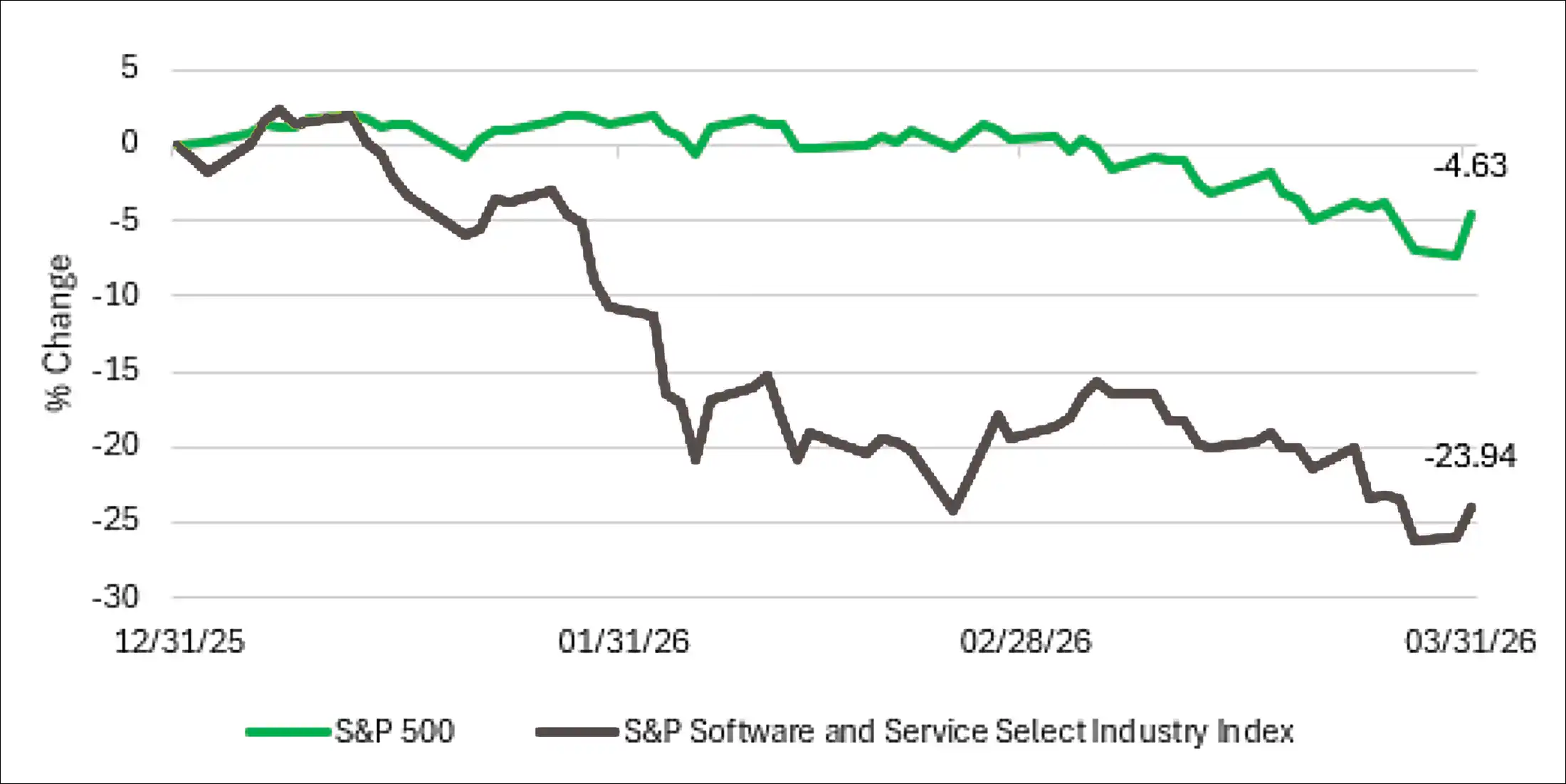

The S&P 500 declined 4.3% in the first quarter of 2026, driven primarily by the outbreak of the war in Iran and the resulting surge in oil prices. A less obvious but meaningful contributor to the decline was the historic collapse in software industry stocks. Software stocks in the S&P 500 fell 23.9% in Q1 and underperformed the index by the most in decades (see Figure 1 – next page).[1] The software selloff began last fall and accelerated early this year with the release of agentic artificial intelligence (AI) software coding tools.[2] The central issue is that AI may threaten the profit margins and business models of many software companies by enabling customers to build their own software. AI continues to be a driving force for the economy and for markets driven by data center capital expenditure and the monetization of agentic AI. However, we must consider which companies and industries are most vulnerable to disruption and which are positioned to be beneficiaries.

Woodstock clients are well positioned because our software stock holdings tend to operate as platforms, dominate their industries, and have strong cash flow. As always, we remain disciplined through periods of uncertainty and won’t waver from owning well-constructed, diversified portfolios of high-quality companies, even amidst market swings.

Figure 1: Software Industry v S&P 500 Index Total Return

Sources:-FactSet

Software Disruption Could Spell Trouble for Lenders

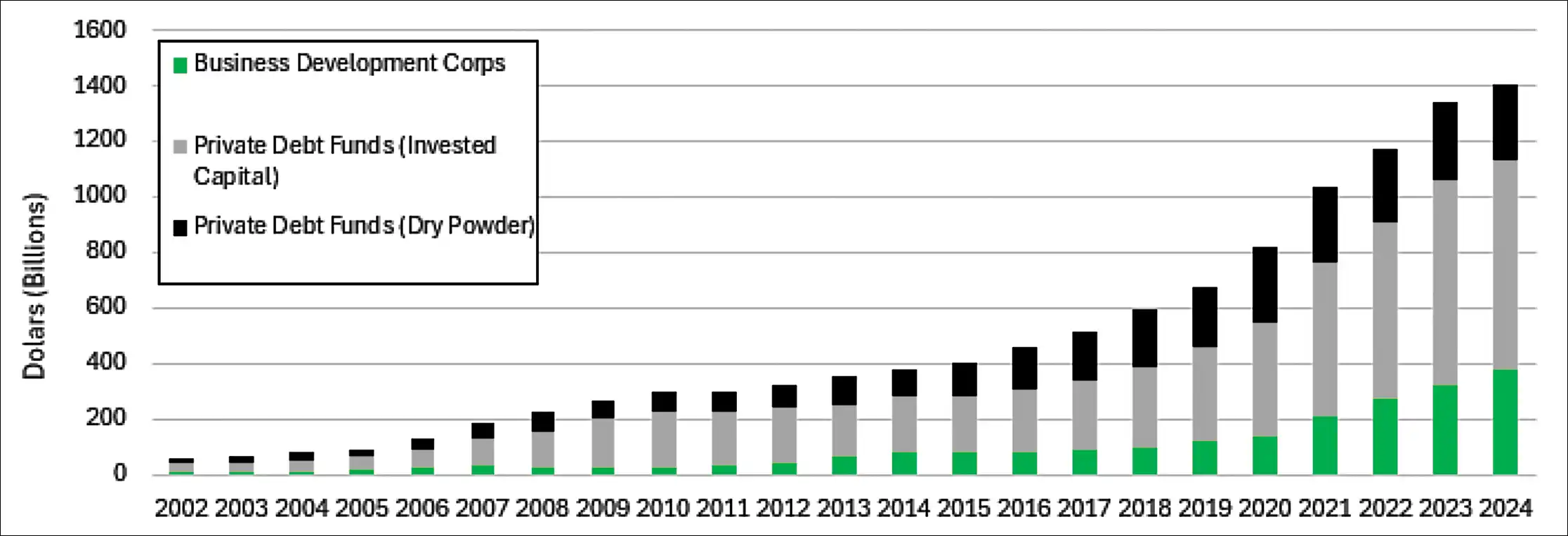

Software companies often have consistent recurring revenue streams, high margins, and low fixed capital needs. These attractive characteristics have driven investments from private capital providers into software companies over the last decade. In fact, software and technology companies accounted for roughly 25% of the private credit market through year-end 2025.[3] Private credit is a form of lending where lenders work directly with borrowers to originate privately held loans. Following the global financial crisis in 2008 and the associated capital rules for banks, private credit loans filled a lending void, growing over 14% per year and

currently standing at $1.8 trillion. This makes the loan category larger than the $1.5 trillion US high-yield bond market and roughly on par with the $1.7 trillion syndicated loan market. [4] Despite its growth, the private credit market represents only ~9% of total corporate borrowing and pales in comparison to investment grade bonds and residential mortgage securities, each totaling around $13 trillion.[5]

Figure 2: Assets Under Management at Private Credit Vehicles

Sources:-Jose Berrospide et al. (2025). “Bank Lending to Private Credit: Size, Characteristics, and Financial Stability Implications,” FEDS Notes. Washington: Board of Governors of the Federal Reserve System, 5/23/25.

The AI disruption narrative has already triggered a wave of loan write-downs and redemption requests across private credit funds. In March 2026, JPMorgan preemptively marked down the value of loans to software companies held as collateral for its private credit lending. Even before realized losses materialize, some private credit funds have been forced to limit redemptions as investors sought to exit illiquid positions.

Default rates of private loans across all industries remain within historical norms for now, but the underlying credit fundamentals should be monitored closely. Weakening covenants, rising payment-in-kind (PIK) usage, generous private ratings, and mark-to-model opacity collectively mask the true extent of borrower stress and risk amplifying losses if the credit cycle turns down. The growing push to distribute private credit to retail investors adds another layer of risk as well.

Notwithstanding rising concerns about defaults, the Federal Reserve’s June 2025 banking system stress test concluded that private credit loans do not pose a systemic risk to the US economy. Further, the banks that Woodstock clients are invested in have limited exposure to private credit markets and are generally well capitalized should defaults materialize. In our Winter 2024 QMP, we noted there was “too much private equity capital chasing too few good investment ideas and PE firms are responding by loading up companies with risky debt to return cash to investors.” Our views towards private investments have not changed, and we will remain focused on investing in high-quality US stocks for our clients.