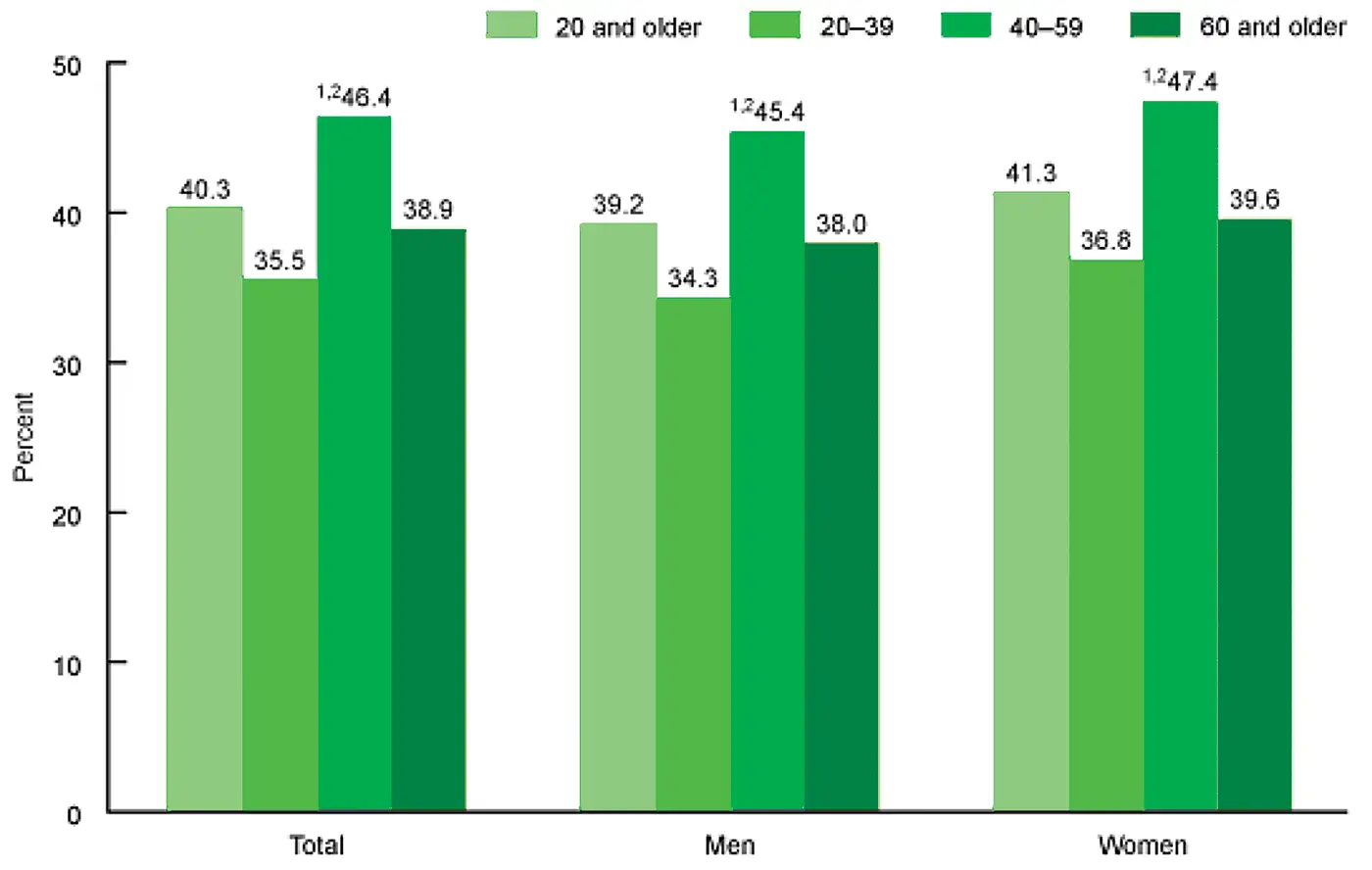

According to the US Centers for Disease Control (CDC), in 2023 more than 40% of US adults were obese with prediabetes or had Type II diabetes (see Figure 1). Some estimates indicate that the measure is rapidly approaching 70%.

Obesity and diabetes are serious metabolic diseases with pronounced comorbidities that have substantial personal and economic costs. The latter include the untoward downstream consequences of heart disease and a host of chronic diseases. All these contribute to higher rates of early mortality and high benefits expenses as well as reduced economic productivity.

Figure 1 – Percentage of US Adults with Obesity with Prediabetes or Type II Diabetes

Source: www.cdc.gov/obesity/data-and-statistics

The pharmaceutical industry has responded to the crisis with the development of GLP-1 drugs. This class of drugs operates to trigger insulin release by the pancreas and to reduce the release of glucose (sugar) into the blood. The drugs need to be administered under the guidance of a physician. Treatment starts at a low dosage and is adjusted up or down as individuals respond.

Initially GLP-1s were primarily for diabetes and dosed by injections, but now a much wider range of medical indications is evolving and oral forms (pills) are becoming available. The uptake of the drugs has been dramatic and is expected to remain so well into the next decade (see Figure 2).

Figure 2

Source: Grandview Research

The GLP-1s are marketed under a variety of brand names, including Ozempic, Mounjaro, Zepbound, and Wegovy. The FDA-approved iterations of these mediations are from Eli Lilly and Novo Nordisk, but more are on the horizon.

A Competitive Market

Given the size of the market and its expected growth, many competitors are angling for a piece of the action. This includes almost all the major drug companies, but these are well behind Lilly and Novo, which seem to have the advantage of a substantial head start with large multipronged forward-looking R&D programs and manufacturing facilities. However, there still appears to be plenty of room for new competitors to gain profitable niches.

Many marginal entities have entered the market. These offer deeply discounted drug look-alikes while treading on patent laws. Most of these iterations lack clinical data that supports claims of efficacy or safety. Indeed, many are sourced in China or India and often contain impurities and poorly controlled chemical elements.

The GLP-1s offer potential weight loss in the middle teens percentage. However, side effects include nausea and diarrhea which, over time, should moderate, but sagging skin and muscle loss can be significant negatives, especially for older patients. Maintaining weight loss benefits requires lifetime usage by the patient.

Industry Prospects

Wall Street is modeling future global GLP-1 annual revenues exceeding $100 billion. Since competitive factors and government pressures are acting to reduce prices of these medications, realizations are likely to fall short of projections. Still, operating margins (and earnings) should remain robust as R&D spending on related drugs moderates, distribution costs (pharmacy benefit manager discounts) are rationalized, and manufacturing efficiencies are realized. Revenues from a plethora of drugs for downstream maladies are likely to augment the GLP market.

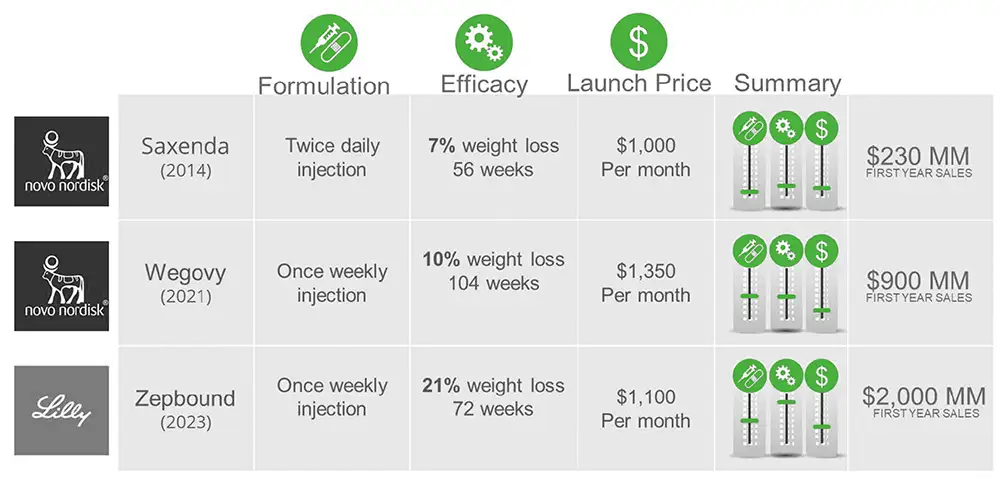

The weight loss drugs are expensive, with the current list price of GLP-1s for individuals in the $1,000 per month range (see Figure 3). However, only the uninsured few pay the full price. Many of the latter often turn to marginal marketers, taking on the risks of poor quality and efficacy. Even with declining prices, the poor and uninsured will not be able to afford the drugs.

Figure 3 – GLP-1 Prices

Source: OZMOSI

Burgeoning weight loss and related costs are stressing the already stressed US healthcare system. Insurance companies are responding by increasing prices and reducing or terminating coverage. As discussed above, drug companies have begun reducing prices (but hope to maintain margins) through direct-to-consumer sales. States are beginning to cut related Medicaid coverage.

In coming years, the GLP-1 landscape is up for significant change. The major pharma companies are pouring significant resources into R&D and acquisitions to improve and expand their weight loss portfolios. Independent research entities (often funded by private equity) are attempting to find new therapies. Successful researchers are likely to be acquired by large companies.

Notwithstanding lower unit prices, the increasing utilization of weight loss and related drugs will continue to stress budgets. Still, these drugs do have the potential to truncate the obesity crisis. The GLP-1s cut morbidity-associated obesity, thus reducing system costs. At least as important, emergent therapies for downstream diseases will contribute mightily to stabilizing costs and mortality from many diseases. Thus, much as antibiotics drugs did in the mid-20th century, this new class of drugs could make significant contributions to the US health system.

— Peter C. Hartzel, Senior Vice President